The COVID-19 pandemic has seen market volatilityVolatilityA statistical measure of the dispersion of returns for a given investment. This is used by investors as a standard measurement of risk i.e. generally higher volatility is viewed as higher risk. read more rise to unprecedented highs throughout March and has tested the resilience and strength of our investment process.

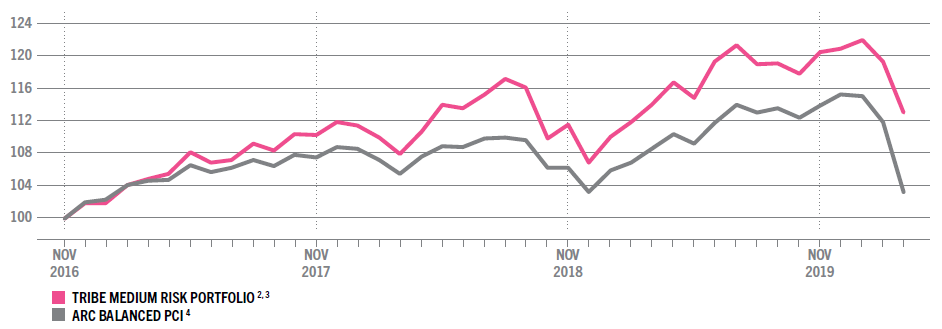

It was only three months ago, we released Tribe’s three-year performance highlighting our investment approach and our strong risk-adjusted performance. Our results showed that we had outperformed within our comparable universe (as defined by ARC) by 6.7% during this period. We attribute this to prioritising investment into companies that are being more thoughtful about future-proofing their earnings, and consequently, their own corporate brands.

We believe by consistently and rigorously adhering to our twin-lensTwin-lensTribe’s two separate assessments of an investment’s financial and impact credentials — the potential monetary returns it may deliver as well as its social and environmental outcomes. read more (investment and impact) investment selection approach, we’re able to deliver both financial and non-financial returns to our clients.

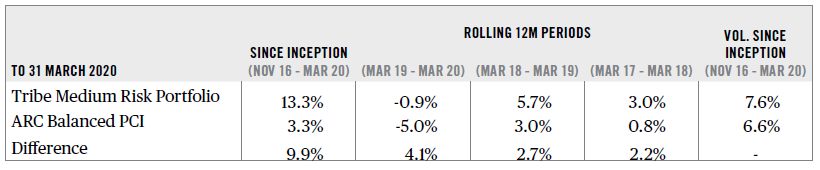

Despite the challenging market conditions, our Q1 2020 performance shows continued relative outperformance, which up until now, has been delivered in the comparatively benign environment of a pre-Covid-19 world. Our medium-risk bespoke model performance fell -6.6% in Q1, versus -10.6% for ARC1.

Return metrics

There are three major themes adding to our performance:

- Within our Strategic Asset Allocation, we have a relatively high (21%) exposure to “uncorrelated/alternative” investments which we class as those investments which have revenue and earnings models uncorrelated to the liquid equityEquityThe universe of traded company shares. Investments can fluctuate according to market conditions, the performance of individual companies and that of the broader equity market. read more and creditCreditSynonymous with fixed income – securities where the security issuer is obligated to repay investors the amount they borrowed plus an interest margin. read more markets. Our investments in social housingSocial housingHousing provided for the disadvantaged or with specialised requirements, usually funded by local or central government. read more and battery storageBattery storageThe capturing and storing of green energy that isn’t needed at the time of generation and is saved until it’s needed. read more recorded gains in the Q1 2020 period. We believe that our focus on impactful and positive investments helps us in uncovering and researching many of these types of opportunities.

- We carry minimal exposure to the travel and tourism industries, as well as the non-staple consumer goods businesses. Our preference is for businesses geared towards solutions addressing and supporting the UN Sustainable Development Goals. In addition, we benefitted from being overweight, relative to the index, in healthcare and utilities names, which have fared considerably better on a relative basis.

- We have a near zero exposure to fossil fuel energy stocks. While portfolios such as ours received a relative boost from the failure of the Saudi/Russian oil production discussions mid quarter, we note that oil prices were already suffering from lower demand from China based on the Covid-19 disruption before settling at now half their H2 2019 average levels.

The Covid-19 crisis is a test of our investment thesis. This period of heightened market volatilityVolatilityA statistical measure of the dispersion of returns for a given investment. This is used by investors as a standard measurement of risk i.e. generally higher volatility is viewed as higher risk. read more, and of course human tragedy, is driving an evolution in the assessment of what constitutes appropriate corporate behaviour. Our performance over this period provides the team here at Tribe further conviction that businesses which have already re-focussed their culture to (i) take into account the broad goals of the sustainabilitySustainabilityMeeting today’s needs without compromising the ability of future generations to meet their needs, by working towards the attainment of the UN SDGs. read more agenda, and/or (ii) are working towards solutions that are focused on creating greater balance in both society and the environment, are investing in their long-term relevance and hence, ultimate value to all shareholders.