Australian bushfires, record global temperatures, the Black Lives Matter movement and Covid-19; H1 2020 has seen environmental, societal and financial disruption on an unprecedented scale. This has presented an opportunity for companies and investors to take pause and consider how things could change and how things should change.

Disruption accelerates change. The increase in societal and environmental stress over the past decade has gradually been gaining investor attention, corporate participation and policy leadership in areas of responsible and sustainable practice. The events of Q1 have accelerated this attentions towards better business practices.

Q2 saw a rapid and broad-based rebound in equityEquityThe universe of traded company shares. Investments can fluctuate according to market conditions, the performance of individual companies and that of the broader equity market. read more and creditCreditSynonymous with fixed income – securities where the security issuer is obligated to repay investors the amount they borrowed plus an interest margin. read more markets. But as the market recovery gained pace, it became increasingly evident that while Covid-19 has affected everyone, it has not affected everyone equally, and as a consequence, many governments heeded calls to “build back better” and greener. Throughout the quarter, many European countries announced policies attuned to promoting more responsible corporate behaviour. Denmark, for example, was an early mover in declaring that its state financial support package would not be available to companies registered in offshore tax havens. Similarly, France attached environmental conditionality to some of its fiscal measures including the airline industry.

More than ever, impact investing is providing a targeted way to channel wealth into building back a better society and environment. Identifying the companies, managers and solutions that are working towards maintaining a floor for society’s needs while respecting the environmental ceiling. Our methodology supports those companies investing in the “base of the pyramid”. For example, the provision of health, housing, utilities and food, sectors where earnings have been generally protected and where we have held overweight positions.

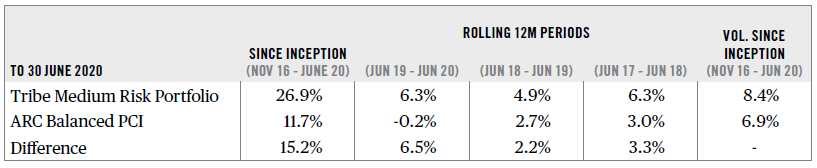

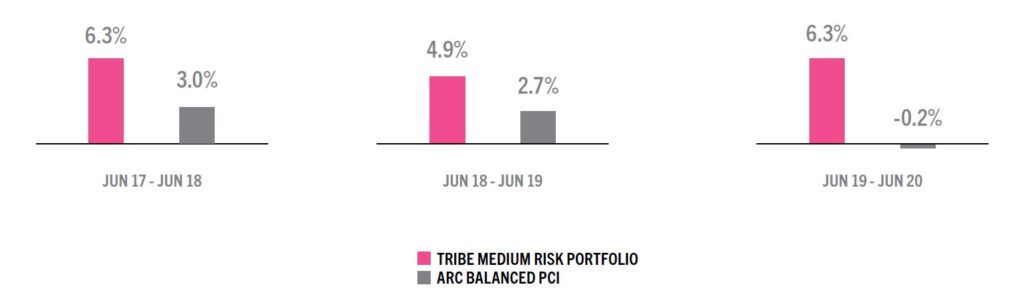

Our medium risk bespoke model portfolio has outperformed more than 15%* since November 2016, relative to ARC¹, with more than half of this outperformance occurring in H1 2020 through Covid-19 related market turmoil.

Return Metrics*

Discrete annual performance4

Looking forward

By embedding impact considerations into our investment decisions, we remain focused on the longer term as we move through a particularly volatile start to 2020. This focus has prevented the temptation towards knee jerk selling, and reaffirmed the strength of our conviction in backing particular sustainable themes such as clean energy transition and the circular economy.

As we move into H2, we remain disciplined and committed to our longer-term investment themes. We continue to look for ways to diversify our exposure to new opportunities, especially where there is a strong structural growth theme and low correlation to the wider equityEquityThe universe of traded company shares. Investments can fluctuate according to market conditions, the performance of individual companies and that of the broader equity market.

read more and creditCreditSynonymous with fixed income – securities where the security issuer is obligated to repay investors the amount they borrowed plus an interest margin.

read more markets.