At Tribe, we believe impact investing should be considered orthodox, long-term investing. We draw inspiration from learnings from the likes of Warren Buffet and his “forever” investment timeframe and Howard Marks’ “second order” thinking to bolster our methodology. The difference is the emphasis we place in prioritising positive investments that directly contribute to global sustainable development and address a social, economic or environmental issue society is facing.

Over the last few weeks, much has been written about how well ESG strategies have performed through the COVID-19 market crisis. Morningstar, in a detailed study (see Appendix), noted an overall outperformance for ESG labelled strategies. They found this was mainly attributable to an aggregated combination of ESG strategies being underweight in energy, overweight in technology, with further alpha being added by an overall superior stock selection. Of more significance, we believe, COVID-19 has brought to the fore, the businesses that are supporting and driving the world through this crisis. The businesses that are demonstrating their ingrained sustainable practices across all metrics which is allowing them to not only weather the storm but help others to do so also.

While this is a helpful short-term data point; we continue to look ahead at the longer term and focus on refining our process to position ourselves for the metanarrative which we think will define all investing over the course of the next decade. While sceptics may question our “values centric” ways, we believe that our twin-lensTwin-lensTribe’s two separate assessments of an investment’s financial and impact credentials — the potential monetary returns it may deliver as well as its social and environmental outcomes. read more approach (placing equal analysis on both investment and impact opportunities) is the inevitable consequence of a thoughtful application of long-term investment orthodoxy.

So, what does long-term investing actually mean for us? Our investment selection approach, seeks to uncover opportunities that offer strong societal and environmental benefits, in combination with attractive financial attributes. We are looking for well-run businesses or “compounders” who are driving long-term sustainable economic growth and we set our investment timeframe as “forever” (which is made easier given that sustainabilitySustainabilityMeeting today’s needs without compromising the ability of future generations to meet their needs, by working towards the attainment of the UN SDGs. read more considerations feature so heavily for us). For impact or impact agnostic investors this might mean a company with a high purchase regularity or one defending a share in a difficult to contest market.

This may all seem like pretty standard practice, however, the central sustainable theme that we seek to compound happens over time. The current COVID-19 crises and its impact on society demonstrates the intrinsic benefit of a long-term investment approach where sustainabilitySustainabilityMeeting today’s needs without compromising the ability of future generations to meet their needs, by working towards the attainment of the UN SDGs. read more for all corporate stakeholders is taken into account. Over the coming weeks and months, companies will begin to absorb the costs of negative externalitiesExternalitiesAn externality can be both positive or negative and can stem from either the production or consumption of a good or service. An externality is a cost or benefit that isn’t financially incurred or received by the creator. read more which government regulations and society had previously given them privilege to externalise. Being allowed to socialise and have tax-payers pick up the cost of these negative externalitiesExternalitiesAn externality can be both positive or negative and can stem from either the production or consumption of a good or service. An externality is a cost or benefit that isn’t financially incurred or received by the creator. read more clearly benefits some companies – think of a polluter or employer that fails to pay a living wage. Our “second order” thinking, when we ask “and then what?”, drives us to favour those companies who are already recognising the possible consequences to society and applying this either through a combination of their business activities or internal processes, with the former often being a key driver in reinforcing the latter. We believe these companies are positioned to be long-term winners.

The current COVID-19 pandemic should act as a catalyst for companies to re-cast their systemic role and responsibility, or investors will quickly recognise that companies who don’t understand this will, at best, have significant additional costs coming or, at worst, fail to respond and damage their long-term competitiveness. This crisis has already seen governments committing vast sums to help support the economy – they will want a return on their investment. This is providing a timely opportunity to ensure companies cover all the costs of their business that they might otherwise be seeking to socialise. We have already seen the banks, the focus of much outrage given the generous terms of their bail outs during the 2008 financial crisis, noticeably quick to respond to government pressure not to pay their dividend, which suggests some lessons have been learned. There has been a great deal of attention on part of the US airline industry, amongst others, who have been confident they could rely on a government “put” that they have diverted nearly all their recent free cash flow into share buy-backs. It remains to be seen how acceptable future buy-back programmes will be after this crisis passes, given the other potential uses of cash to benefit other corporate stakeholders. The COVID-19 crisis itself, and government and society response to it, needs to compel companies to consider the needs of all stakeholders. Identifying those companies that already understand this, will be the key to identifying the long-term winners.

So, for us at Tribe, we hope that the lesson from Q1 2020 is not only that ESG aligned funds and companies can compete from a returns perspective and even outperform. But also the realisation that a long-term approach, across all sustainable investment metrics, will deliver the best returns for investors, as well as the planet, economy and society.

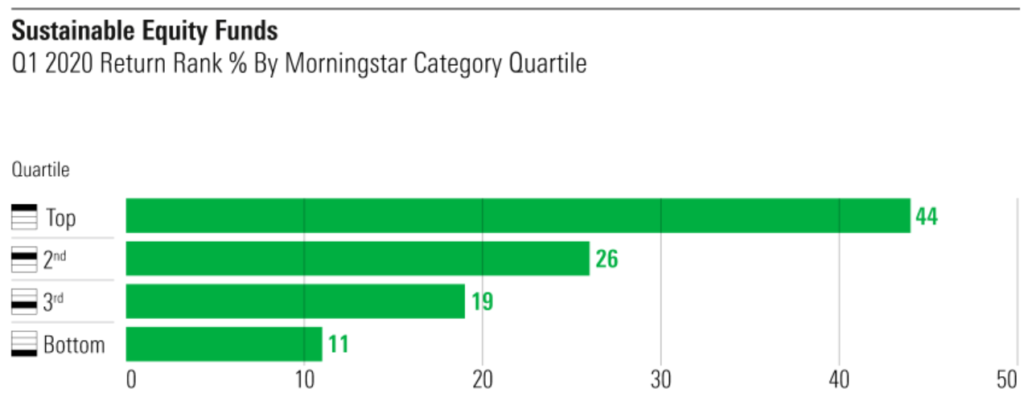

Appendix – Morningstar Direct

During the first quarter, the returns of sustainable equityEquityThe universe of traded company shares. Investments can fluctuate according to market conditions, the performance of individual companies and that of the broader equity market. read more funds were clustered in the top halves of their respective categories, and more sustainable funds’ returns ranked in their category’s best quartile than in any other quartile. The returns of 70% of sustainable equityEquityThe universe of traded company shares. Investments can fluctuate according to market conditions, the performance of individual companies and that of the broader equity market. read more funds ranked in the top halves of their categories and 44% ranked in their category’s best quartile. By contrast, only 11% of sustainable equityEquityThe universe of traded company shares. Investments can fluctuate according to market conditions, the performance of individual companies and that of the broader equity market. read more funds finished in their category’s worst quartile. That’s 4 times more sustainable funds finishing in the best quartile than in the worst quartile of their categories.